Trust Bank Annual Report 1988

Page 1

Contents

2 President’s Report

4 General Manager’s Report

6 Consolidated Profit Statement

Auditor’s Report

7 Consolidated Balance Sheet

8 Statement of Changes in Financial Position

9 Statement of Accounting Policies

10 Notes to the Accounts

12 Directory

Photo caption – New Havelock North Branch premises opened in September 1987

Page 2

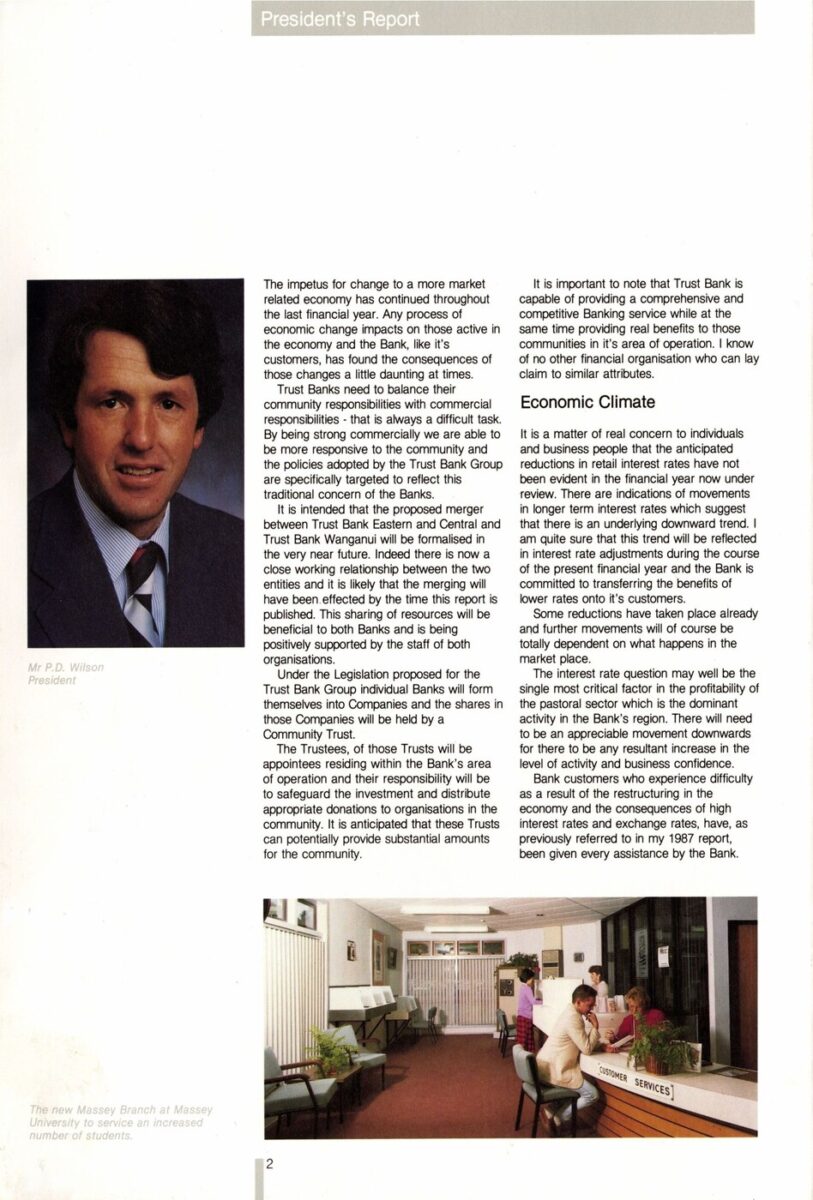

President’s Report

Photo caption – Mr P. D. Wilson

President

The impetus for change to a more market related economy has continued throughout the last financial year. Any process of economic change impacts on those active in the economy and the Bank, like it’s customers, has found the consequences of those changes a little daunting at times.

Trust Banks need to balance their community responsibilities with commercial responsibilities – that is always a difficult task. By being strong commercially we are able to be more responsive to the community and the policies adopted by the Trust Bank Group are specifically targeted to reflect this traditional concern of the Banks.

It is intended that the proposed merger between Trust Bank Eastern and Central and Trust Bank Wanganui will be formalised in the very near future. Indeed there is now a close working relationship between the two entities and it is likely that the merging will have been effected by the time this report is published. This sharing of resources will be beneficial to both Banks and is being positively supported by the staff of both organisations.

Under the Legislation proposed for the Trust Bank Group individual Banks will form themselves into Companies and the shares in those Companies will be held by a Community Trust.

The Trustees, of those Trusts will be appointees residing within the Bank’s area of operation and their responsibility will be to safeguard the investment and distribute appropriate donations to organisations in the community. It is anticipated that these Trusts can potentially provide substantial amounts for the community.

It is important to note that Trust Bank is capable of providing a comprehensive and competitive Banking service while at the same time providing real benefits to those communities in it’s area of operation. I know of no other financial organisation who can lay claim to similar attributes.

Economic Climate

It is a matter of real concern to individuals and business people that the anticipated reductions in retail interest rates have not been evident in the financial year now under review. There are indications of movements in longer term interest rates which suggest that there is an underlying downward trend. I am quite sure that this trend will be reflected in interest rate adjustments during the course of the present financial year and the Bank is committed to transferring the benefits of lower rates onto it’s customers.

Some reductions have taken place already and further movements will of course be totally dependent on what happens in the market place.

The interest rate question may well be the single most critical factor in the profitability of the pastoral sector which is the dominant activity in the Bank’s region. There will need to be an appreciable movement downwards for there to be any resultant increase in the level of activity and business confidence.

Bank customers who experience difficulty as a result of the restructuring in the economy and the consequences of high interest rates and exchange rates, have, as previously referred to in my 1987 report, been given every assistance by the Bank.

Photo caption – The new Massey Branch at Massey University to service an increased number of students

Page 3

Photo caption – The Bank was a major supporter of the Central Districts Cricket Association and the one day international was an outstanding success at McLean Park, Napier.

Growth of Deposits

A record year for the Bank. Funds on deposit increased by $114,209,000 bringing the total funds held by the Bank to $333,921,000. A growth of some 52%. I am delighted with this continuing support from our community lending. With the appreciable growth of funds the Bank has been in a position to fully meet it’s customers housing loan requirements. All loans which have met the Bank’s criteria, have been advanced. There have been some additional funds which we have been able to lend in the commercial sector following a liberalisation of the Legislation previously limiting commercial advances. Total of new Trustees loans granted during the year amount to $119,000,000

Profit

I am pleased to report a very satisfactory result on a much increased funds base. A return of 1.6% on average assets enables us to maintain a satisfactory level of investment in the Bank’s future and this year we have bought to account unrealised gains in Fixed Interest Securities. These securities have appreciated in value following a movement downwards in wholesale interest rates particularly during the latter part of this financial year. Our profit for the year is therefore made up as follows.

Operating Profit $3,632,000

Plus gains on fixed interest securities and Government stock $5,754,000

$9,386,000

Less Taxation $4,659,000

Company Profit $25,000

Net profit $4,752,000

Stabilty in the market will reduce the prospect of gains on fixed interest securities The Bank will therefore be relying on it’s operating profit which, needs to be maintained at the present modest level.

Bad Debts

The Bank has limited debt exposure which is to be expected given its investment in housing finance.

Provisions made in the statement of accounts follow a very careful examination of the Bank’s investments, and cover all known and contingent debts.

Donations

There is to be an increase in the amount to be distributed this year and I am pleased to advise that the Trustees have granted an amount of $200,000 for the 1988 year. In addition the Bank has participated in the $50,000 already distributed through the Trust Bank Group to those suffering as a result of the recent cyclone disaster in the Wairoa and Gisborne districts

In the relatively short history of the Bank donations and special grants now total in excess of $1,000,000.00.

Board of Trustees

Last year I referred to the need for trustees to give more of their time to the Bank and a continuation of a high level of participation has been required through 1988. I am grateful for the support of all the Board and in particular my Deputy Mr N. J Toomey.

Mr D. F. McLeod and R. J. Burns completed their five year terms in 1987 and I acknowledge the contribution they have made to the Bank over their many years of service. New appointments to the Board this year were Mr B. Parker and Mr J. A. Cornelius.

Staff

The merger with Wanganui will give a combined Bank staff of about 400 people. To be effective those people need to work as a team and the accomplishments of the Bank over the last twelve months are evidence of good working relationships and a very solid team effort. On behalf of the Board I extend my thanks to all members of the staff.

Ewing Robertson is to retire later this year. As the Bank’s Chief Executive Ewing Robertson must take considerable credit for the achievements of the Bank and for it’s growth from small beginnings in 1964 to what is now a real financial force in the community. The Board joins me in thanking Ewing Robertson and his management team for their efforts over the last year.

P. D. Wilson

PRESIDENT

Page 4

Chief Executive’s Report

Photo caption – Mr E. Robertson

Chief Executive

The writing of this report is significant in two ways. Firstly, the publishing of these accounts brings to an end the most exciting and progressive period this Bank has experienced. Secondly, the opportunity with the merging with Trust Bank Wanganui will enable us to provide an enhanced banking service to a significant region.

This will create new challenges, but the Bank is confident it has the products, services, people and management to offer a competitive service to its customers.

Retail Network

The creating of two separate regional offices, Northern and Southern was very successful and necessary. It has provided better communications and the ability to address problems at branch level. During the year two new Branches were established in Palmerston North, one at Massey University and the other in the central business district. Havelock North Branch was modernised and major improvements carried out at others to ensure our customers receive the best possible service.

Treasury/Money Market Operation

In August 1987 our Money Market Department accepted its first Corporate deposit. Prior to that the Department was restricted to servicing short to medium term investments to private individuals and carrying out the Treasury function of the Bank. The acceptance of our service by the Corporate sector with deposits regularly in excess of $30 million, has justified the commitment to the latest technology and the allocation of resources in this specialist area.

Foreign Exchange

In the second year of operation this development has continued to expand and made a good contribution to the Bank’s earnings.

Commercial Banking

A growing part of the Bank’s business. The Bank has now diversified at a steady rate to provide a full financial service to all sectors of our community.

Travel Operation

In line with the Bank’s policy of extending this service the Bank has purchased Vogue Travel in Wanganui as an extension of our Gisborne and Napier operations.

Insurance

Welcome to John Snowling. The introduction of his expertise has added impetus to the promotion of our Insurance services.

For the first time in the Bank’s history, over a million dollars in premium income was paid during the financial year for Trustcover and related Insurance Services.

With an ever increasing portfolio and exciting enhancements to existing products, Trustcover insurances will continue to enjoy a favourable position in a very competitive market.

Community Involvement

Despite all the changes taking place within Trust Bank, no compromise has been made to the longstanding commitment to be Bankers for the region it serves. The return of profits to the community will be carried into the future through a Community Trust for the Eastern and Central region. $200,000 will be allocated to Donations from 1987/88 tax paid profits.

This year the Bank was a major sponsor of the Central Districts Cricket Association with whom we are looking forward to a continuing close association. The provision of funds for Sponsorship is important and it is necessary that these limited funds be used to best advantage

Marketing

The overall marketing of the Bank‘s services to customers has been good and the implementation of the TRUST BANK Corporate Identity has been professional and thorough. Although this Bank has a reasonable market share of “main bank” customers there is tremendous opportunity to increase this. The Bank commissioned ‘Business and Economic Research Limited’ to carry out an indepth study of its area and the findings have been very promising. The growth and prosperity of the East Coast and Central North Island through to 1991 is very positive and the Bank feels confident of its future.

Page 5

Tribute

Because this is my last message as Chief Executive of Trust Bank Eastern and Central I would like to express my thanks to the Board for their valued guidance. To the staff my very special thanks in what was a demanding year.

The changes brought about by deregulation of the finance sector continue to consume the efforts of all Management and Staff. I cannot speak too highly of the commitment given willingly to ensure that the Bank remains a strong force into the future. The pressures have been compounded by technological changes arising from our involvement in the Trust Bank Group, the imminent merger with Wanganui and the pending legislation changes affecting Trust Bank.

It is clear to me that the new management structure has the ability to grasp the undoubted opportunities that will present themselves and the dedication to carry them through for the benefit of the Bank.

The Public can be confident that our staff will continue to give to them the best possible service. A new era of banking will emerge that will secure Trust Bank Central as a major force in a highly competitive banking environment. The benefit ultimately will go to the community. This is where the Bank started and it will be the motivating force of the future

After 17 years as Chief Executive I retire before the end of the year. It gives me great comfort to be leaving with the knowledge that the Bank will be going into the future with confidence.

E. Robertson

CHIEF EXECUTIVE

Photo captions –

(Top) Money Market personnel Nancy Neal and Lew Kenah

(Left) International personnel Walker Knight (left) and Barrie Petersen.

Page 6

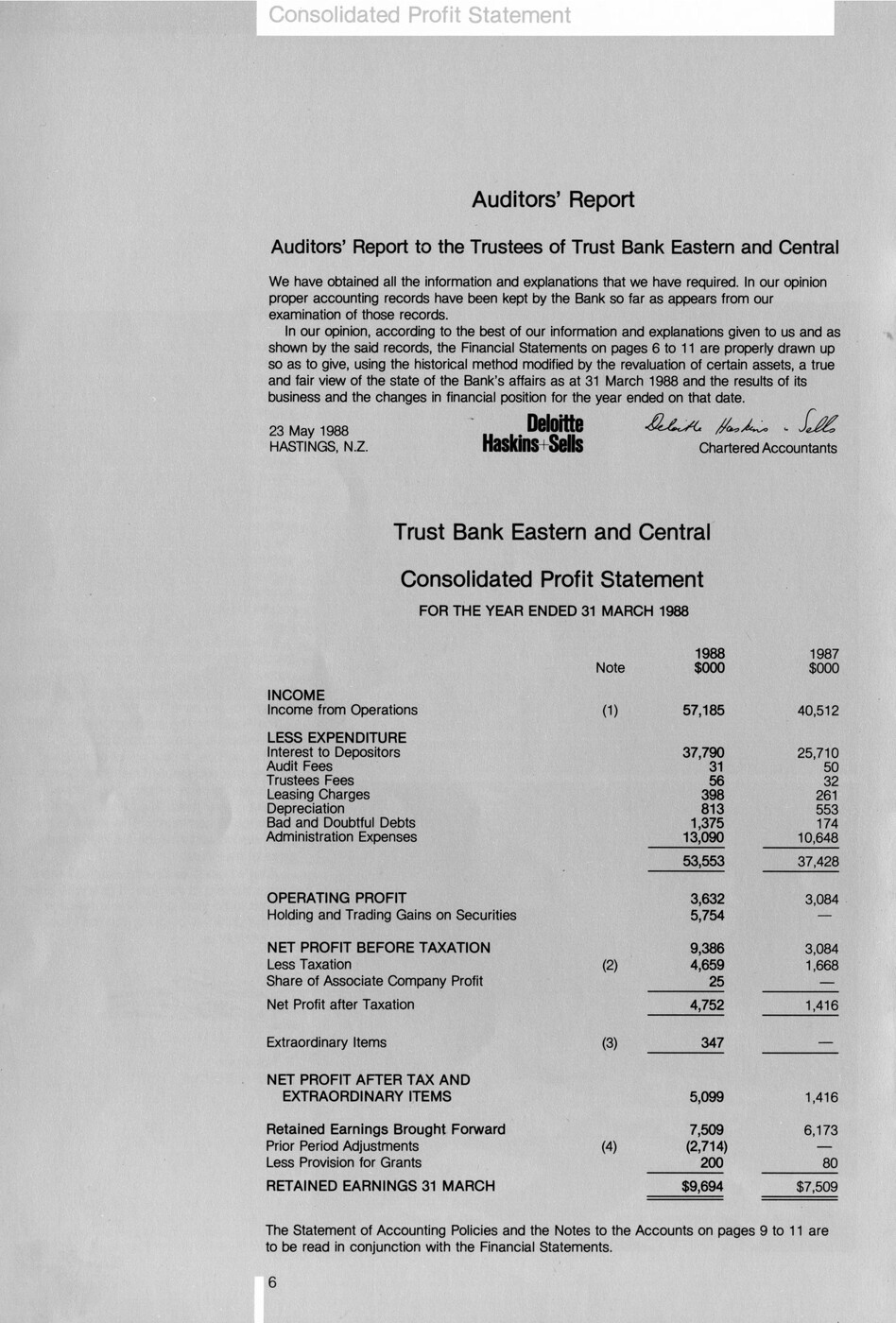

Consolidated Profit Statement

Auditors’ Report

Auditors’ Report to the Trustees of Trust Bank Eastern and Central

We have obtained all the information and explanations that we have required. In our opinion proper accounting records have been kept by the Bank so far as appears from our examination of those records. In our opinion, according to the best of our information and explanations given to us and as shown by the said records, the Financial Statements on pages 6 to 11 are properly drawn up so as to give, using the historical method modified by the revaluation of certain assets, a true and fair view of the state of the Bank’s affairs as at 31 March 1988 and the results of its business and the changes in financial position for the year ended on that date.

23 May 1988

HASTINGS, N.Z.

Deloitte Haskins +Sells.

Chartered Accountants

Trust Bank Eastern and Central

Consolidated Profit Statement

FOR THE YEAR ENDED 31 MARCH 1988

1988 1987

Note $000 $000

INCOME

Income from Operations (1) 57,185 40,512

LESS EXPENDITURE

Interest to Depositors 37,790 25,710

Audit Fees 31 50

Trustees Fees 56 32

Leasing Charges 398 261

Depreciation 813 553

Bad and Doubtful Debts 1,375 174

Administration Expenses 13,090 10,648

53,553 37,428

OPERATING PROFIT 3,632 3,084

Holding and Trading Gains on Securities 5,754 –

NET PROFIT BEFORE TAXATION 9,386 3,084

Less Taxation (2) 4,659 1,668

Share of Associate Company Profit 25 –

Net Profit after Taxation 4,752 1,416

Extraordinary Items (3) 347 –

NET PROFIT AFTER TAX AND EXTRAORDINARY ITEMS 5,099 1,416

Retained Earnings Brought Forward 7,509 6,173

Prior Period Adjustments (4) (2,714) –

Less Provision for Grants 200 80

RETAINED EARNINGS 31 MARCH $9,694 $7,509

The Statement of Accounting Policies and the Notes to the Accounts on pages 9 to 11 are to be read in conjunction with the Financial Statements.

Page 7

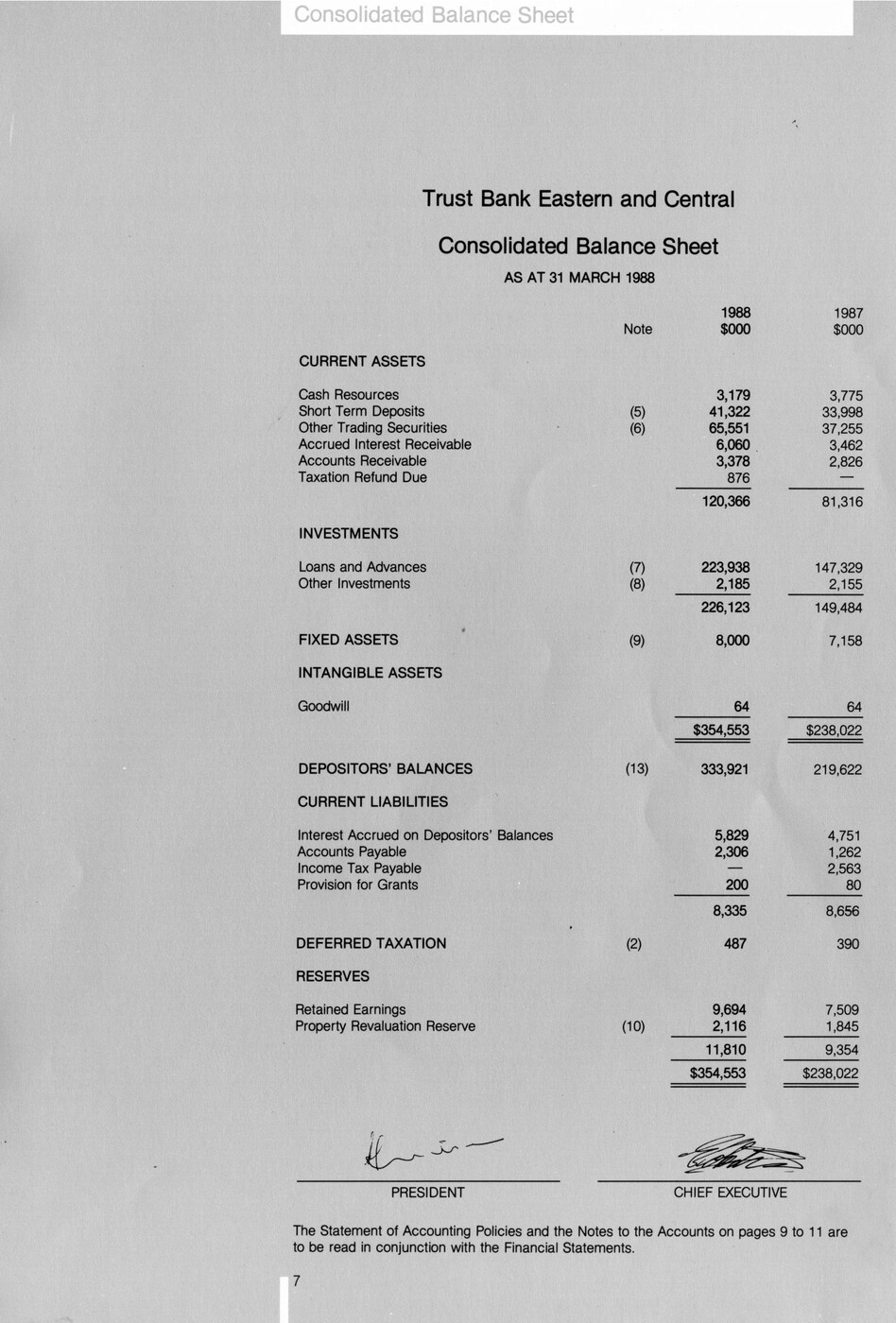

Consolidated Balance Sheet

Trust Bank Eastern and Central

Consolidated Balance Sheet

AS AT 31 MARCH 1988

1988 1987

Note $000 $000

CURRENT ASSETS

Cash Resources 3,179 3,775

Short Term Deposits (5) 41,322 33,998

Other Trading Securities (6) 65,551 37,255

Accrued Interest Receivable 6,060 3,462

Accounts Receivable 3,378 2,826

Taxation Refund Due 876 –

120,366 81,316

INVESTMENTS

Loans and Advances (7) 223,938 147,329

Other Investments (8) 2,185 2,155

226,123 149,484

FIXED ASSETS (9) 8,000 7,158

INTANGIBLE ASSETS

Goodwill 64 64

$354,553 $238,022

DEPOSITORS’ BALANCES (13) 333,921 219,622

CURRENT LIABILITIES

Interest Accrued on Depositors’ Balances 5,829 4,751

Accounts Payable 2,306 1,263

Income Tax Payable – 2,563

Provision for Grants 200 80

8,335 8,656

DEFERRED TAXATION (2) 487 390

RESERVES

Retained Earnings 9,694 7,509

Property Revaluation Reserve (10) 2,116 1,845

11,810 9,354

$354,553 $238,022

PRESIDENT CHIEF EXECUTIVE

The Statement of Accounting Policies and the Notes to the Accounts on pages 9 to 11 are to be read In conjunction with the Financial Statements.

Page 8

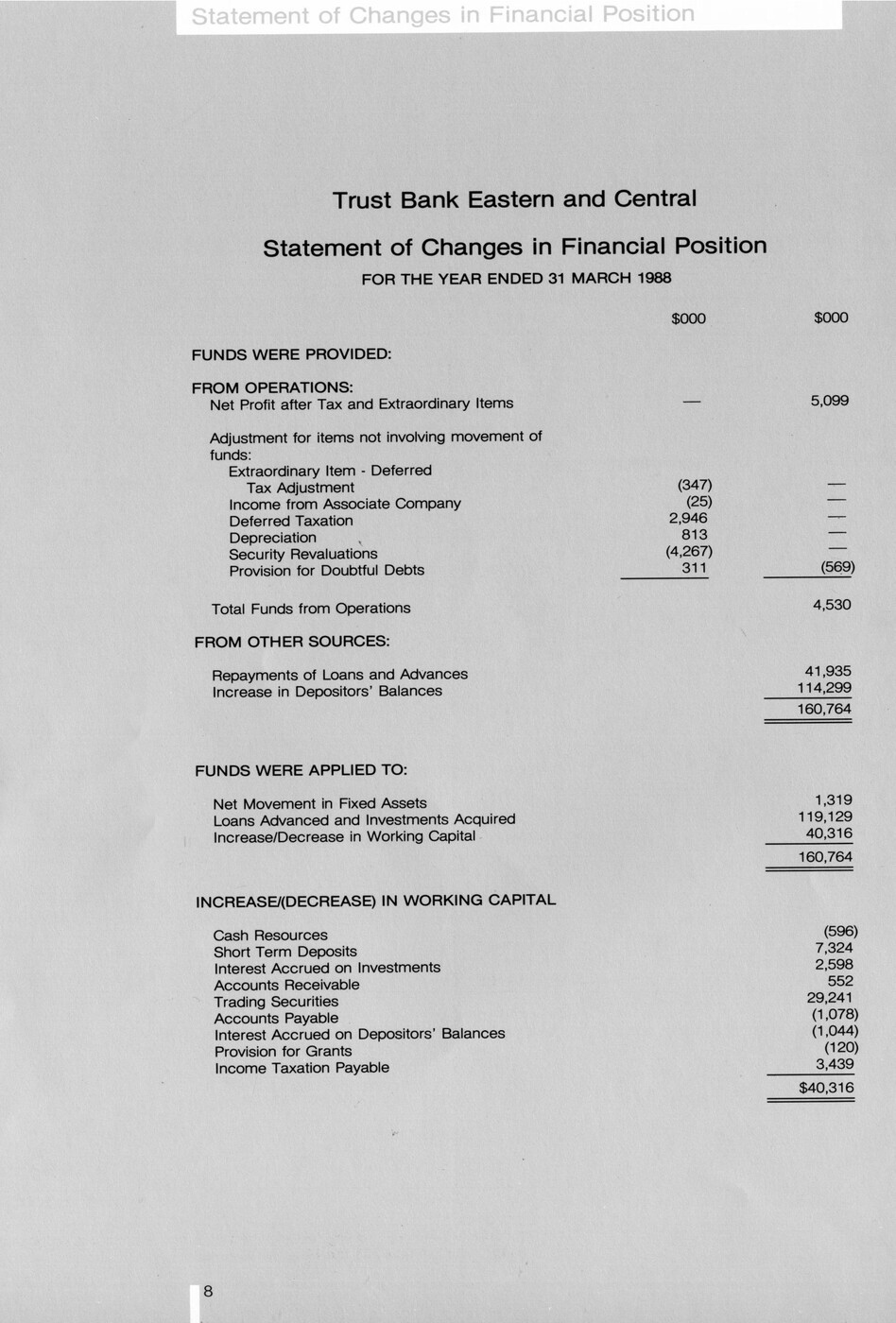

Statement of Changes in Financial Position

Trust Bank Eastern and Central

Statement of Changes in Financial Position

FOR THE YEAR ENDED 31 MARCH 1988

$000 $000

FUNDS WERE PROVIDED

FROM OPERATIONS:

Net Profit after Tax and Extraordinary items – 5,099

Adjustment for items not involving movement of funds:

Extraordinary item – Deferred Tax Adjustment (347) –

Income from Associate Company (25) –

Deferred Taxation 2,946 –

Depreciation 813 –

Security Revaluations (4,267) –

Provision for Doubtful Debts 311 (569)

Total Funds from Operations 4,530

FROM OTHER SOURCES:

Repayments of Loans and Advances 41,935

Increase in Depositors’ Balances 114,299

160,764

FUNDS WERE APPLIED TO:

Net Movement in Fixed Assets 1,319

Loans Advanced and Investments Acquired 119,129

Increase/Decrease in Working Capital 40,316

160,764

INCREASE/(DECREASE) IN WORKING CAPITAL

Cash Resources (596)

Short Term Deposits 7,324

Interest Accrued on Investments 2,598

Accounts Receivable 552

Trading Securities 29,241

Accounts Payable (1,078)

Interest Accrued on Depositors’ Balances (1,044)

Provision for Grants (120)

Income Taxation Payable 3,439

$40,316

Page 9

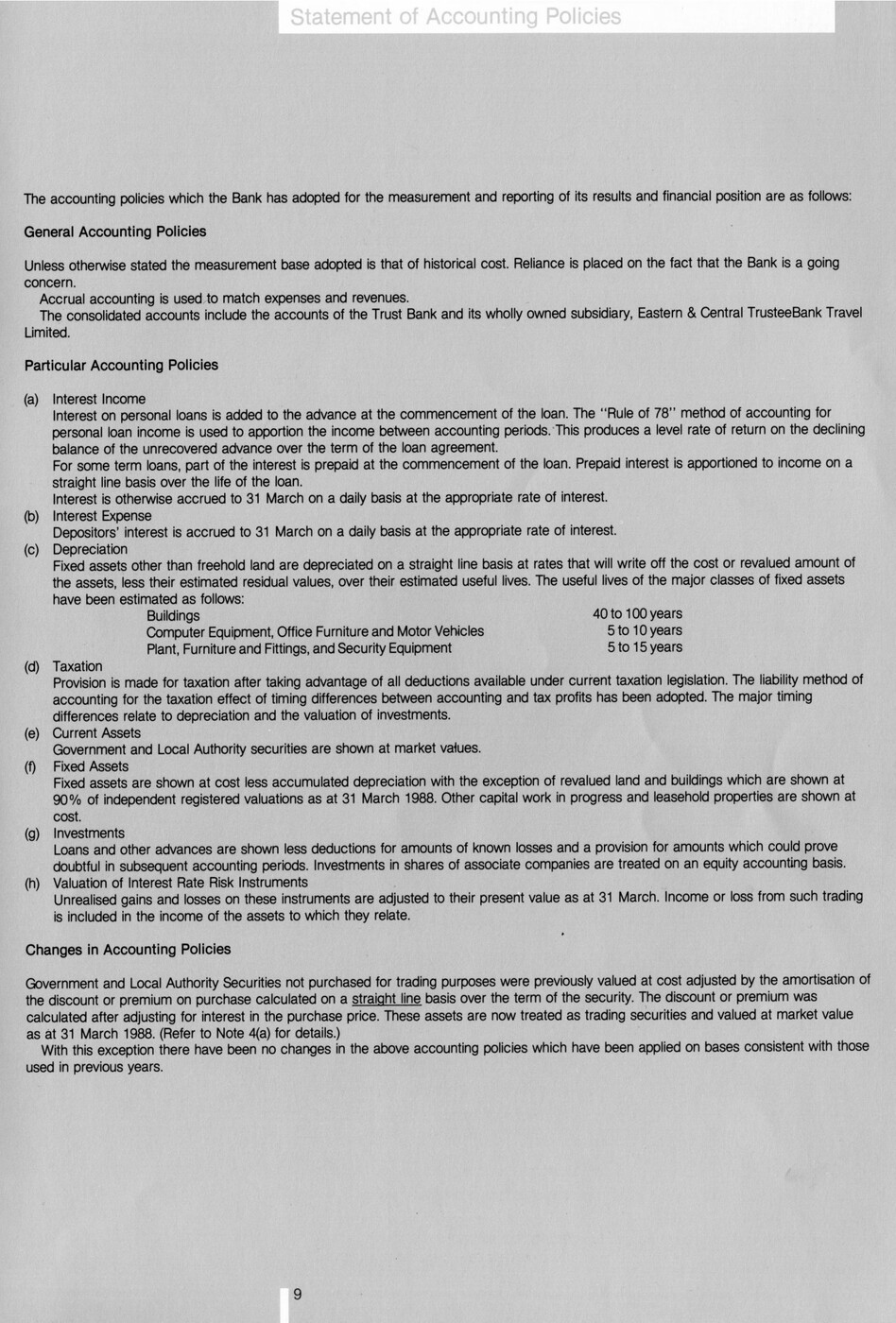

Statement of Accounting Policies

The accounting policies which the Bank has adopted for the measurement and reporting of its results and financial position are as follows:

General Accounting Policies

Unless otherwise stated the measurement base adopted is that of historical cost. Reliance is placed on the fact that the Bank is a going concern.

Accrual accounting is used to match expenses and revenues.

The consolidated accounts include the accounts of the Trust Bank and its wholly owned subsidiary, Eastern & Central TrusteeBank Travel Limited.

Particular Accounting Policies

(a) Income Interest

Interest on personal loans is added to the advance at the commencement of the loan. The “Rule of 78” method of accounting for personal loan income is used to apportion the income between accounting periods. This produces a level rate of return on the declining balance of the unrecovered advance over the term of the loan agreement.

For some term loans, part of the interest is prepaid at the commencement of the loan. Prepaid interest is apportioned to income on a straight line basis over the life of the loan.

Interest is otherwise accrued to 31 March on a daily basis at the appropriate rate of interest.

(b) Interest Expense

Depositors’ interest is accrued to 31 March on a daily basis at the appropriate rate of interest.

(c) Depreciation

Fixed assets other than freehold land are depreciated on a straight line basis at rates that will write off the cost or revalued amount of the assets, less their estimated residual values, over their estimated useful lives. The useful lives of the major classes of fixed assets have been estimated as follows:

Buildings 40 to 100 years

Computer Equipment, Office Furniture and Motor Vehicles 5 to 10 years

Plant, Furniture and Fittings, and Security Equipment 5 to 15 years.

(d) Taxation

Provision is made for taxation after taking advantage of all deductions available under current taxation legislation. The liability method of accounting for the taxation effect of timing differences between accounting and tax profits has been adopted. The major timing differences relate to depreciation and the valuation of investments

(e) Current Assets

Government and Local Authority securities are shown at market values.

(f) Fixed Assets

Fixed assets are shown at cost less accumulated depreciation with the exception of revalued land and buildings which are shown at 90% of independent registered valuations as at 31 March 1988. Other capital work in progress and leasehold properties are shown at cost.

(g) Investments

Loans and other advances are shown less deductions for amounts of known losses and a provision for amounts which could prove doubtful in subsequent accounting periods. Investments in shares of associate companies are treated on an equity accounting basis.

(h) Valuation of Interest Rate Risk Instruments

Unrealised gains and losses on these instruments are adjusted to their present value as at 31 March income or loss from such trading is included in the income of the assets to which they relate.

Changes in Accounting Policies

Government and Local Authority Securities not purchased for trading purposes were previously valued at cost adjusted by the amortisation of the discount or premium on purchase calculated on a straight line basis over the term of the security. The discount or premium was calculated after adjusting for interest in the purchase price. These assets are now treated as trading securities and valued at market value as at 31 March 1988. (Refer to Note 4(a) for details.)

With this exception there have been no changes in the above accounting policies which have been applied on bases consistent with those used in previous years.

Page 10

Notes to the Accounts

Note 1988 1987

$000 $000

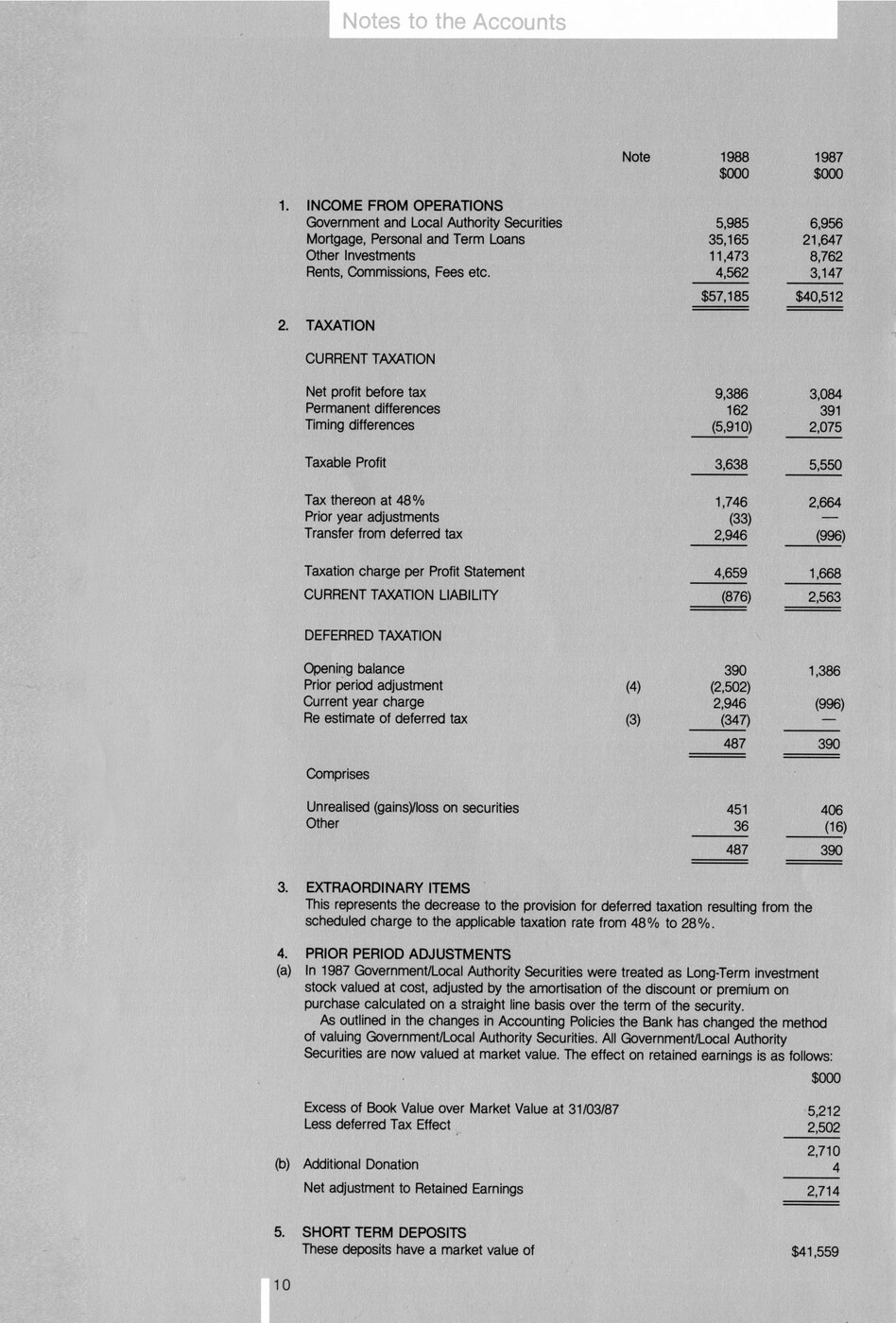

1. INCOME FROM OPERATIONS

Government and Local Authority Securities 5,985 6,956

Mortgage, Personal and Term Loans 35,165 21,647

Other investments 11,473 8,762

Rents, Commissions, Fees etc. 4,562 3,147

$57,185 $40,512

2. TAXATION

CURRENT TAXATION

Net profit before tax 9,386 3,084

Permanent differences 162 391

Timing differences (5,910) 2,075

Taxable Profit 3,638 5,550

Tax thereon at 48% 1,746 2,664

Prior year adjustments (33) –

Transfer from deferred tax 2,946 (996)

Taxation charge per Profit Statement 4,659 1,668

CURRENT TAXATION LIABILITY (876) 2,563

DEFERRED TAXATION

Opening balance 390 1,386

Prior period adjustment (4) (2,502) –

Current year charge 2,946 (996)

Re estimate of deferred tax (3) (347) –

487 390

Comprises

Unrealised (gains)/loss on securities 451 406

Other 36 (16)

487 390

3. EXTRAORDINARY ITEMS

This represents the decrease to the provision for deferred taxation resulting from the scheduled charge to the applicable taxation rate from 48% to 28%.

4. PRIOR PERIOD ADJUSTMENTS

(a) In 1987 Government/Local Authority Securities were treated as Long-Term investment stock valued at cost, adjusted by the amortisation of the discount or premium on purchase calculated on a straight line basis over the term of the security.

As outlined in the changes in Accounting Policies the Bank has changed the method of valuing Government/Local Authority Securities. All Government/Local Authority Securities are now valued at market value. The effect on retained earnings is as follows:

$000

Excess of Book Value over Market Value at 31/03/87 5,212

Less deferred Tax Effect 2,502

2,710

(b) Additional Donation 4

Net adjustment to Retained Earnings 2,714

5. SHORT TERM DEPOSITS

These deposits have a market value of $41,559

Page 11

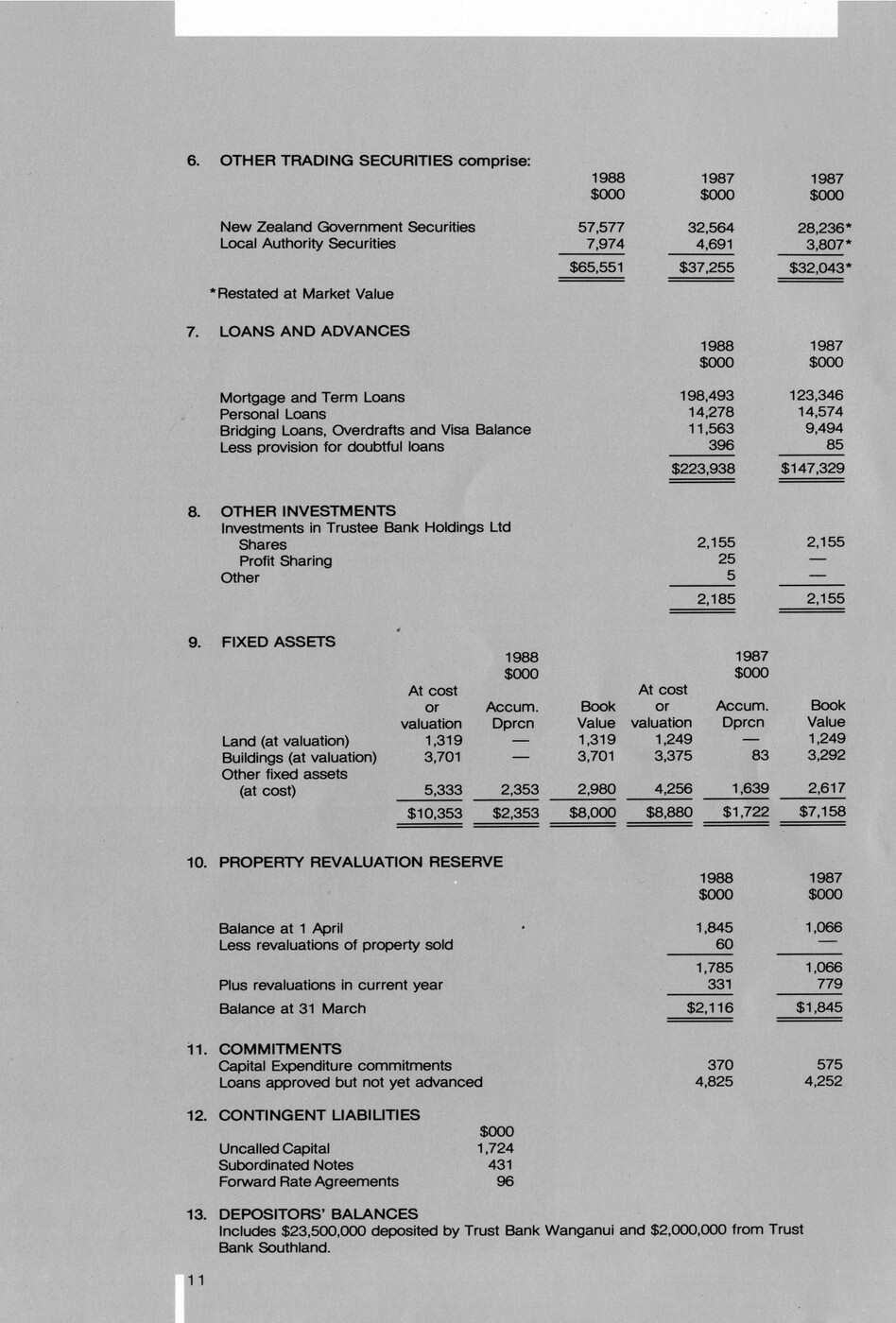

6. OTHER TRADING SECURITIES comprise:

1988 1987 1987

$000 $000 $000

New Zealand Government Securities 57,577 32,564 28,236*

Local Authority Securities 7,974 4,691 3,807*

$65,551 $37,255 $32,043*

*Restated at Market Value

7. LOANS AND ADVANCES

1988 1987

$000 $000

Mortgage and Term Loans 198,493 123,346

Personal Loans 14,278 14,574

Bridging Loans, Overdrafts and Visa Balance 11,563 9,494

Less provision for doubtful loans 396 85

$223,938 $147,329

8. OTHER INVESTMENTS

Investments in Trustee Bank Holdings Ltd

Shares 2,155 2,155

Profit Sharing 25 –

Other 5 –

2,185 2,155

9. FIXED ASSETS

1988 1987

$000 $000

At cost or Valuation Accum. Dprecn. Book Value At cost or Valuation Accum. Dprcn Book Value

Land (at valuation) 1,319 – 1,319 1249 – 1,249

Buildings (at valuation) 3,701 – 3,701 3,375 83 3,292

Other fixed assets

(at cost) 5,333 2,353 2,980 4,256 1,639 2,617

$10,353 $2,353 $8,000 $8,880 $1,722 $7,158

10. PROPERTY REVALUATION RESERVE

1988 1987

$000 $000

Balance at 1 April 1,845 1,066

Less revaluations of property sold 60 –

1,785 1,066

Plus revaluations in current year 331 779

Balance at 31 March $2,116 $1,845

11. COMMITMENTS

Capital Expenditure commitments 370 575

Loans approved but not yet advanced 4,825 4,252

12. CONTINGENT LIABILITIES

$000

Uncalled Capital 1,724

Subordinated Notes 431

Forward Rate Agreements 96

13. DEPOSITORS’ BALANCES

Includes $23,500,000 deposited by Trust Bank Wanganui and $2,000,000 from Trust Bank Southland.

Page 12

Directory

Board of Trustees

PRESIDENT: Mr P. D. Wilson, A. C. A.

DEPUTY PRESIDENT: Mr N. J. Toomey, LLB.

TRUSTEES: Mr J. E. Bolderson

Mr. R. N. Carter, M. B. E., B. Com. A. C. A.

Mr. J. A. Cornelius, B. Com., F. C. A.

Mr M. E. C. Cox, A. C. A.

Mr N. J. Foote

Mr F. B. Hopwood, A.C.A.

Mrs A. F. King, M. P.

Mr D. H. Miller, J. P., F. C. A.

Mr. B. Parker, A.C.A.

Mr J. R. M. Wills, J. P.

Executive Management

Ewing Robertson J. P., Chief Executive

Kevin Wilson Assistant General Manager – Retail Banking

Nancy Neal Assistant General Manager – Finance

Richard Cook Assistant General Manager – Administration

Photo caption – John Snowling (standing) who heads Insurance services for the Bank with Pat Sloane, Banking Services Manager

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Original digital file

RobertsonE894_TrustBankAnnualReport1988.pdf

Non-commercial use

This work is licensed under a Attribution-NonCommercial 3.0 New Zealand (CC BY-NC 3.0 NZ).

Commercial Use

The donor of this material does not allow commercial use.Can you help?

The Hawke's Bay Knowledge Bank relies on donations to make this material available. Please consider making a donation towards preserving our local history.

Visit our donations page for more information.

Subjects

Business / Organisation

Trust Bank Eastern and CentralFormat of the original

BookletDate published

1988People

- J E Bolderson

- R J Burns

- R N Carter

- Richard Cook

- J A Cornelius

- M E C Cox

- N J Foote

- F B Hopwood

- A F King

- D F McLeod

- D H Miller

- Nancy Neal

- B Parker

- Ewing Robertson

- Pat Sloane

- John Snowling

- N J Toomey

- J R M Wills

- Kevin Wilson

- P D Wilson

Accession number

894/2060/44768Supporters and sponsors

We sincerely thank the following businesses and organisations for their support.

Do you know something about this record?

Please note we cannot verify the accuracy of any information posted by the community.